Dairy Reduces Risk of Metabolic Syndrome 💪

MARKET NEWS

Daily Dairy Report | April 14, 2026

Dairy Reduces Risk of Metabolic Syndrome 💪

Over the past few weeks, the dairy industry received mixed news. On April 1, the powerful American Heart Association (AHA) released its new dietary guidelines. AHA typically updates its guidelines every five years after reviewing current medical research, and this year it left its guidelines virtually unchanged on everything, including dairy. Despite a growing body of research that shows dairy fat may not contribute to cardiovascular disease and could have a neutral or even protective effect on the heart, AHA continues to recommend that consumers choose low-fat or fat-free dairy products to promote heart health.

At the same time, research published in March showed a compelling link between eating more calcium-rich products, including dairy, and a lower risk of developing metabolic syndrome in adults. Those with metabolic syndrome have a combination of conditions, including high blood pressure, high fasting blood sugar, excess belly fat, and high levels of bad cholesterol and triglycerides, which can significantly increase the risk of heart disease, stroke, and type 2 diabetes. The research, a systematic review and meta-analysis of current research, was published in the journal Nutrients. It examined the relationship between either calcium intake and/or dairy consumption and the prevalence of metabolic syndrome in adults. The results indicated that higher dietary calcium intake was inversely associated with the odds of developing metabolic syndrome, particularly in women. The authors further suggested that calcium could be an important mediator of the cardiometabolic benefits of dairy consumption.

The good news for dairy is that even though AHA did not change its recommendations, research continues to show the benefits of dairy intake to help ward off a variety of diseases and conditions due to its dense and unique nutritional profile. And a range of dairy products, from nonfat to full-fat, will continue to be available for consumers as they make the best choices for their individual health.

NMPF DAIRY MARKET REPORT

Volume 29 | Issue 3 | March 30, 2026

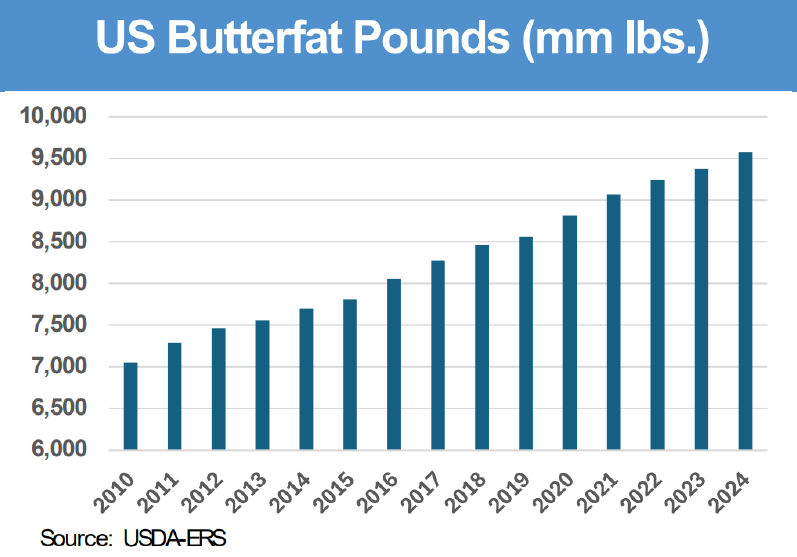

After starting the year in a funk, dairy product prices have noticeably improved even as milk production remains robust, increasing 3.4% in January on a liquid basis. While the milking herd continues to grow, component growth surprisingly decelerated to start 2026, indicating that producers are responding to strong economic incentives from beef-on-dairy but not pushing for maximum milkfat tests with the fall in butter prices. Despite heavy milk production, dairy product supplies and inventories are not overly burdensome. In fact, nonfat dry milk prices are rising due to limited supply, and butter is finding support due to reported low inventories. Domestic demand for dairy proteins remains remarkable, as consumers turn to products like cottage cheese, Greek yogurt and high protein beverages to support health goals. With vigorous domestic protein demand and growing milkfat exports, signs are indicating that the U.S. is moving back towards balance. While DMC margins dipped to $7.81/cwt in January, recent commodity price increases should provide a much-needed boost to margins in the coming months.

READ MORE »

USDA DAIRY MARKET NEWS

April 10, 2026

CHEESE HIGHLIGHTS:

Northeast milk production is in the spring flush, supporting stronger cheese production. Steady retail demand is helping balance lighter bulk interest. Exports remain steady with rising interest from Southeast Asia, and inventories are well balanced. Central milk volumes are plentiful as the spring flush begins, supporting busy post holiday production. Class III spot milk ranges from $7 under to $2 under Class. Cheese output is steady. Demand and export interest remain soft but are expected to improve. In the Western region, strong spring milk output supports steady to stronger cheese production, though spot cheese availability varies and some varieties are tight. Domestic demand ranges from lighter to stronger, food service demand lags other sectors, and export interest holds steady to strong.

BUTTER HIGHLIGHTS:

Stakeholders report that retail demand for butter is generally steady. Some manufacturers note butter sales are up year over year. Bulk butter demand is strong from both domestic and international buyers. Spring flush is resulting in large amounts of milk and cream. However, competing demand from Class II and III manufacturers is keeping cream availability somewhat limited for butter producers. Contractual and spot load intakes at butter production facilities are keeping churns busy seven days a week. Bulk butter overages range from 2 cents below to 7 cents above market across all regions.

FLUID MILK:

Spring flush is in full swing nationwide. Some areas have reached their peak production while other regions are still ramping up. Milkfat is down slightly, but still higher than in recent years. Bottling demand is up in most areas as many educational institutions resume classes after spring break. Class II demand for cream is rising. Ice cream producers are ramping up operations and building inventories for summer. Class III demand is steady. Many cheese makers are increasing manufacturing, some taking in spot loads of milk at a discount. Class III spot prices range from $7-under to $2- under. Class IV demand is steady to strong. Some butter makers are taking in spot volumes of cream to keep churns full. Nonfat dry milk demand remains strong. Condensed skim availability was higher this week. Planned downtime at several plants last week provided additional amounts of condensed skim for the market. As a result, condensed skim was selling at a discount in some areas. Cream multiples for all Classes range:1.15 – 1.42 in the East; 1.00 – 1.27 in the Midwest; 1.06 – 1.28 in the West.

DRY PRODUCTS:

Nonfat dry milk prices were mixed across regions this week. The low/medium heat prices in the Central and East regions declining at the lower end of the range but rising slightly at the upper end, while the mostly range held steady at the low end and moved higher at the top. High heat prices in the Central and East regions increased at the low end and were unchanged at the top, and all price levels in the West strengthened. Dry buttermilk prices firmed across all regions except for the Central and East, where the lower end remained steady. Dry whey markets were steady to higher, led by the largest gain at the bottom of the Central region’s price range. Lactose prices were mostly stable with a slight decrease at the upper end. Production remains steady, but tight inventories continue to limit availability, particularly for higher mesh product. Whey protein concentrate 34% prices were largely steady, with only minor softening at the top of the price range. Dry whole milk strengthened at both ends of the range and continues to trend above year ago levels. Acid and rennet casein prices were unchanged.